Deck Review with Clover Health

Surveying great inventors and businesses

More well thought out work can be found at — https://axial.substack.com/

Axial partners with great founders and inventors. We invest in early-stage life sciences companies often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you — email us at info@axialvc.com

Clover Health is a data-driven health insurance company. The company focuses on Medicare Advantage plans operating a preferred provider organization (PPO). The core premise of Clover is to build patient profiles based on lab tests, health history and more to identify at-risk patients to direct resources and preventive care to.

Founded in 2012 by Vivek Garipalli (private equity and healthcare background) and Kris Gale (was VP of Engineering at Yammer), they took on a hard problem to bring technology to insurance plans for older patients. Whereas peers of Clover at the time were targeting younger patients, the company started building products to reduce hospitalization rates (the name of the game in US healthcare is to make sure a patient doesn’t go to a hospital) and improve care. The company initially focused on intervening earlier for patients with chronic diseases like T2D and congestive heart failure. Over time the purview of the products and business model expanded to where Clover is serving over 50K patients. The long-term vision for Clover is to expand beyond Medicare and begin to develop new medicines and digital products to cure disease.

The first slide of their latest corporate presentation lays out the problem Clover is solving: misaligned incentives in the US healthcare system that increases costs and lowers patient outcomes.

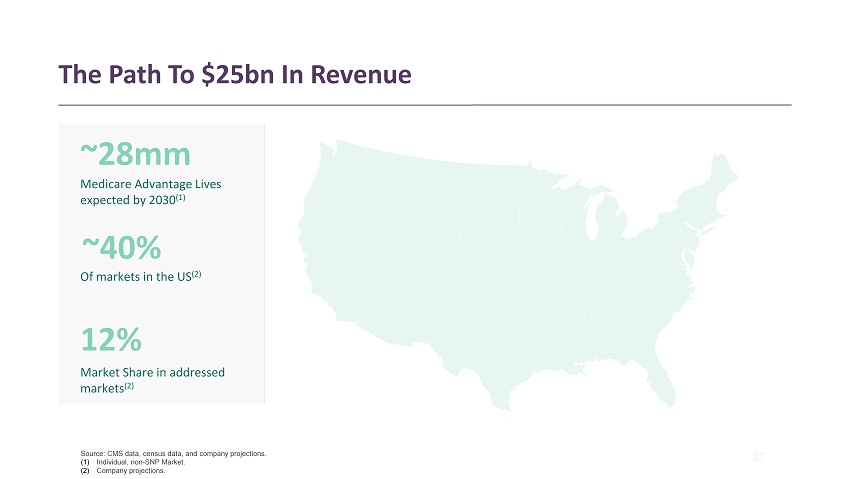

After framing the problem, Clover sizes their market - Medicare plans, which are growing significantly with Baby Boomers joining Medicare increasingly.

With this setup, Clover explains its mission: “to improve every life.” Pretty broad and sets them up to go beyond Medicare and actually make curative products.

Then they highlight their founder-driven team. This implies a longer-term vision and strong ownership culture.

Kind of disjointedly, Clover an increasing market share within Medicare Advantage and revenue.

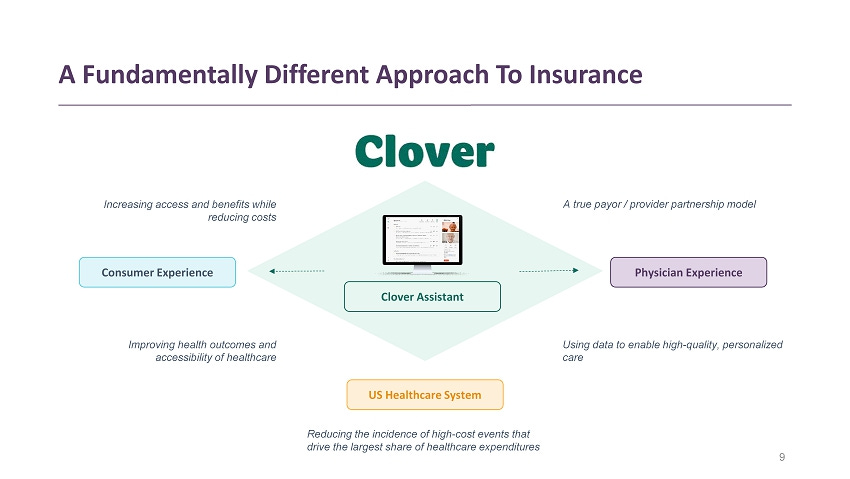

Clover explains their business model, which essentially takes money from the US healthcare system to build software to improve patient (consumer) and physician experiences. The idea is that care quality goes up while costs hopefully come down.

After getting some of the important questions answered, Clover transitions to their value proposition to patients.

The value prop of Clover’s plan is high access and low costs. They frame it as being as accessible at PPOs and cheap at HMOs; this is where software/coordination can make this product profitable.

The company lays ou the cost savings their patients will have - 17%-41%.

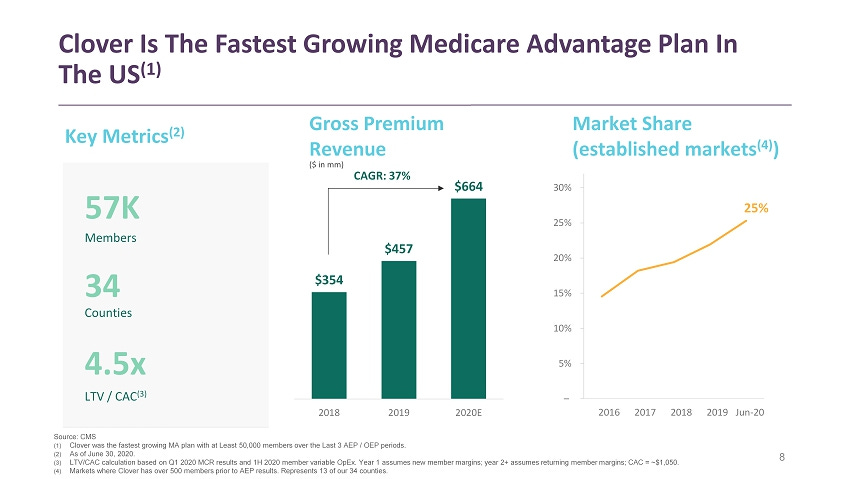

With this cost saving, Clover is the fastest growing Medicare Advantage plan provider over the last 3 years.

After laying out their value prop to patients, Clover does the same for physicians.

Clover helps physicians get paid sooner and more reliably and spend less time scheduling with patients.

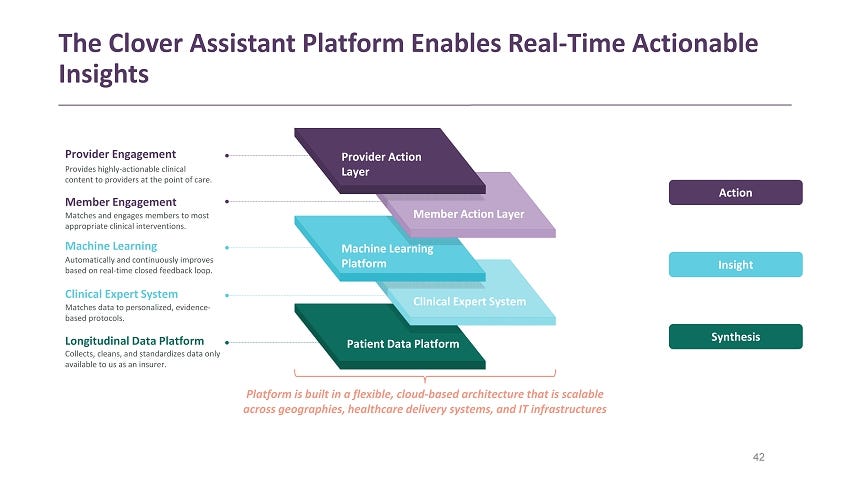

Clover’s Assistant product automates a lot of the tasks around patient follow up and support so physicians can focus on delivering care when needed.

Essentially, Clover Assistant is a software tool to engage with patients and help physicians know when to intervene.

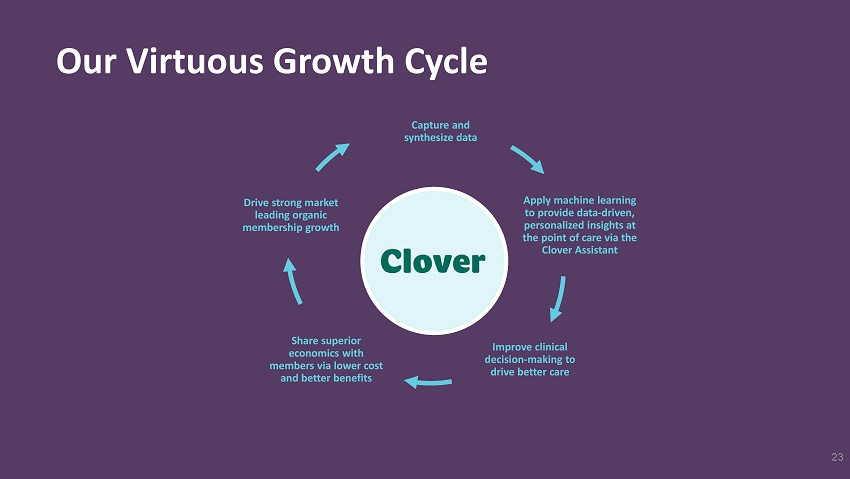

The Assistant product generates a large amount of patients data that Clover wants to apply machine learning in order to predict acute health events and maybe even one day develop drugs to cure them.

With COVID-19, Clover highlights their use of telemedicine.

Clover then provides a case study of how Assistant and preventative care enables them to lower costs.

Product advantages of Assistant: (1) it’s a piece of software (2) NPS is comparable to Netflix (3) they launch new releases pretty frequently.

After explaining their value prop to their two stakeholders, Clover touches upon their growth strategy.

Their growth strategy comes down to reducing costs of care in order to provide lower plan costs that will lead to more patients signing up.

They show that this strategy has led to pretty significant market growth and coverage.

They show that this playbook has been effective in markets they have been in over 4-5 years with market share up to 48% in some areas.

They plan to get to 73K patients by 2021.

With their long-term goal to serve over 1M patients by 2030.

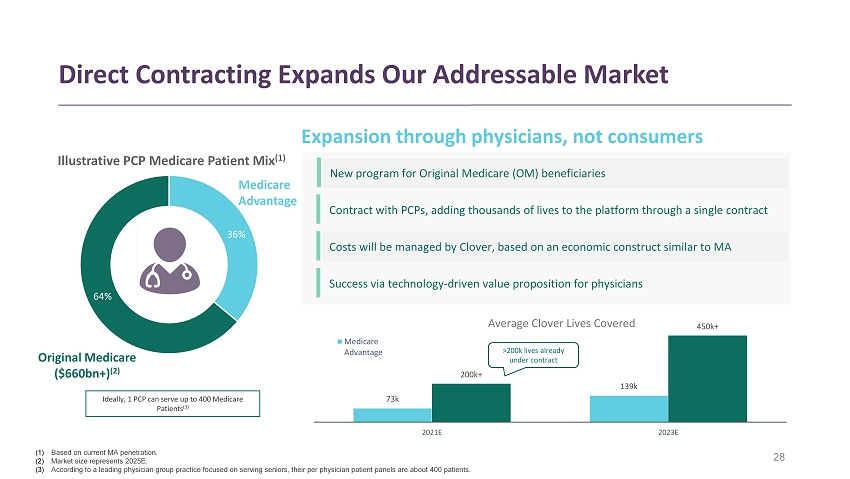

To maintain this growth, Clover will recruit traditional Medicare patients and partner with primary care physician groups to serve their patients.

To complete their presentation, Clover touches on their financials.

The idea is to get to scale and get to profitability. This is highly dependent on the effectiveness of their Assistant product.

This profitability will come from positive unit economics: can Clover keep their patients on their plan and out of hospitals?

With this, the business model of Clover requires retained patients that increase topline revenue without recurring acquisition costs.

Then Clover shows the impact of product development on growth and margins. Their medical cost ratio is already approaching the limit of 80%. I am not sure how they can legally go below 80%; they probably will have to direct the excess toward other projects like drug development.

Clover uses a table to bring their growth and margin goals together.

This is just the table in growth form.

With high-level financials of Clover.

Touching on some of Clover’s advantages - large market and using technology to bring costs down.

The presentation concludes on their SPAC transaction to go public.

With the SPAC acquisition valuing Clover at $3.7B. The best is yet to come.

Clover also uses an appendix.

They have a fancy slide on their Assistant product.

Then how software enables Clover to scale to more patients.

Clover also touches on the positive product impact and negative patient impact of COVID-19.

The deck is pretty comprehensive. Starting off characterizing its market and business model, Clover did a great job at segmenting its two customers: patients and physicians and explaining their value proposition to each.

Follow up questions for the team:

After achieving an 80% MCR, how will Clover use the excess savings? Drug development with Clover Therapeutics? Anything else?

How will the contracts look between Clover and PCPs? Will Clover own the patient relationship? Data rights?

What logic does Clover use to pick new markets to enter? Why has penetration been so high in the Hudson market? Excess marketing or strong value prop?