Deck Review with Danimer Scientific

Deck Review with Danimer Scientific

Surveying great inventors and businesses

More well thought out work can be found at — https://axial.substack.com/

Axial partners with great founders and inventors. We invest in early-stage life sciences companies often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you — email us at info@axialvc.com

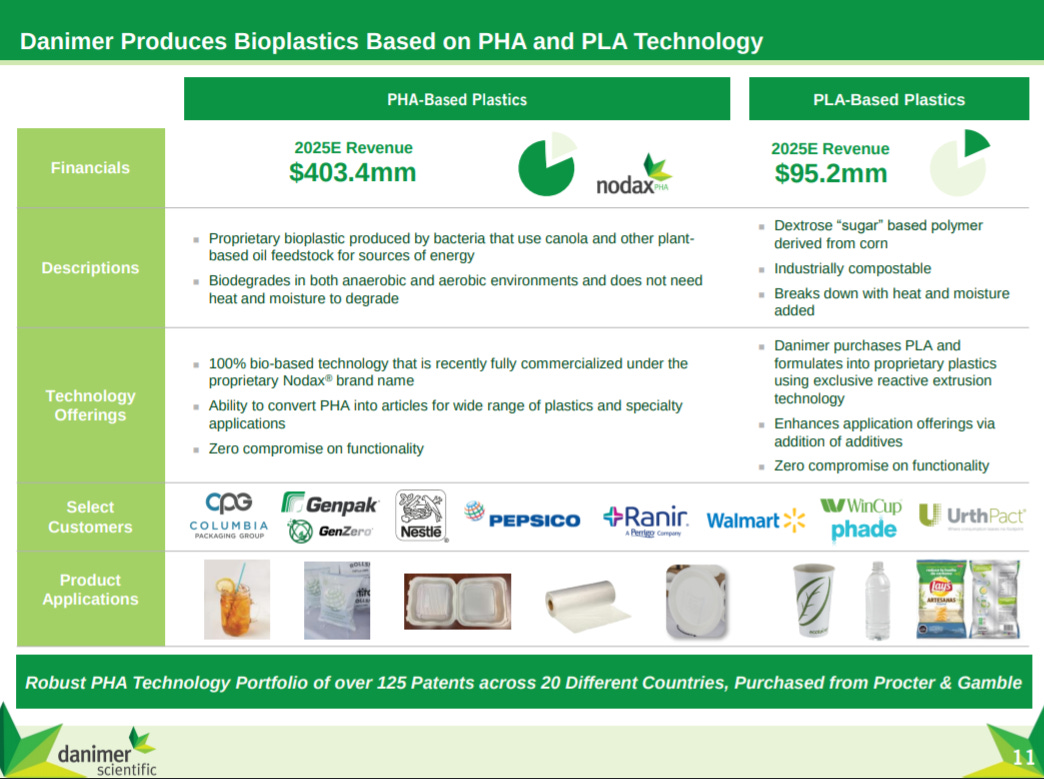

Danimer Scientific was founded in 2004 to develop and commercialize bioplastics. In 2014, the company merged with their supplier, Meredian. That same year, the company’s first bioplastic was approved by the FDA. Danimer’s lead product, Nodax polyhydroxyalkanoates (PHA), a compostable and biodegradable material in fresh and marine water, soil, and anaerobic environments (the degradation time is highly temperature dependent).The company actually was focused on corn-based polylactic acid (PLA); however, in 2007, Danimer acquired IP from Procter & Gamble for their medium-chain-length PHA technology that ultimately became Danimer’s flagship Nodax product. The company has a large bioplastic manufacturing facility in Winchester, Kentucky producing Nodax to produce products like straws, packaging, and containers for companies like PepsiCo, Nestlé, Genpak, WinCup, Columbia Packaging Group, and Plastic Suppliers. With over $40M in revenue (4 customers represent over 60% of sales), Danimer is positioned to scale up bioplastics production and power a shift in consumer and industrial products.

The company’s core technology platform is around functionalizing biopolymers like PLA and PHA, which are sourced from lactic acid and starches respectively and using microorganisms to make them. The current plastic industry generates $10Bs of sales with over 95% of plastics made from fossil fuels. Danimer’s opportunity is to bring technology to develop a substitute for petroleum-based plastics.

The first slide of their latest corporate presentation shows an example of Danimer’s biodegradable plastic product.

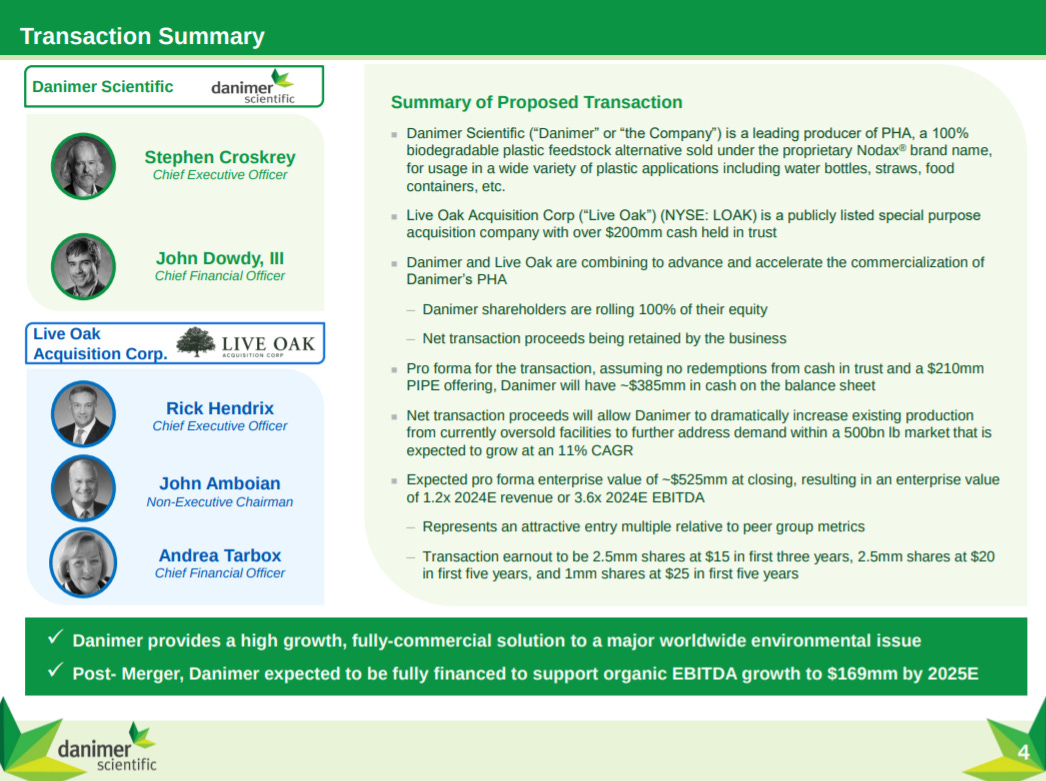

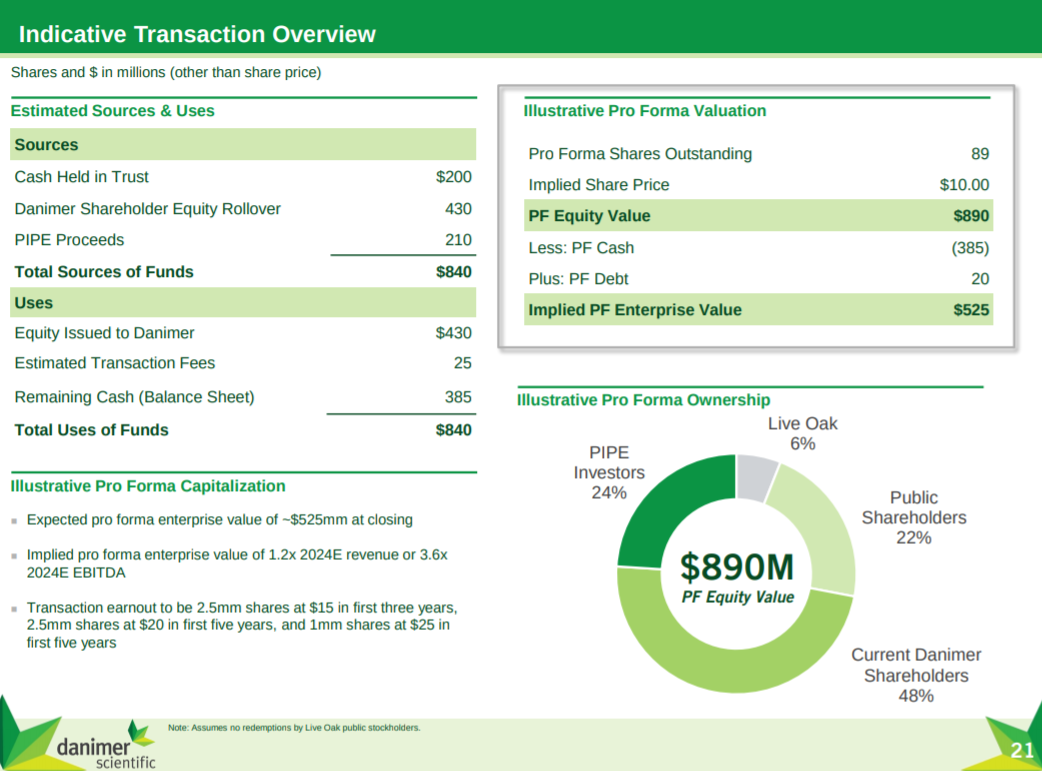

The next slide goes into the SPAC that took Danimer public. Live Oak Acquisition Corp put up $200M with other funds like Apollo Global Management Federated Hermes committing $210M to value the company at around $890M.

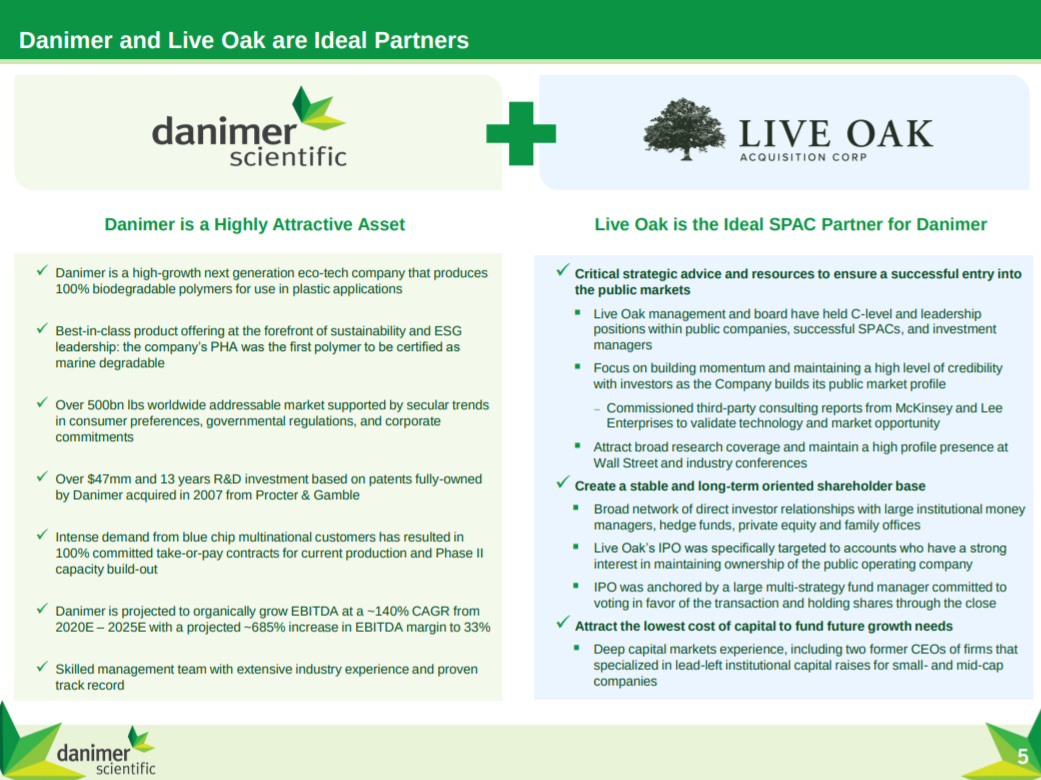

This slide makes the argument on why Danimer is a good SPAC target - growing market, leadership in bioplastics, and in the early-stages of generating sales.

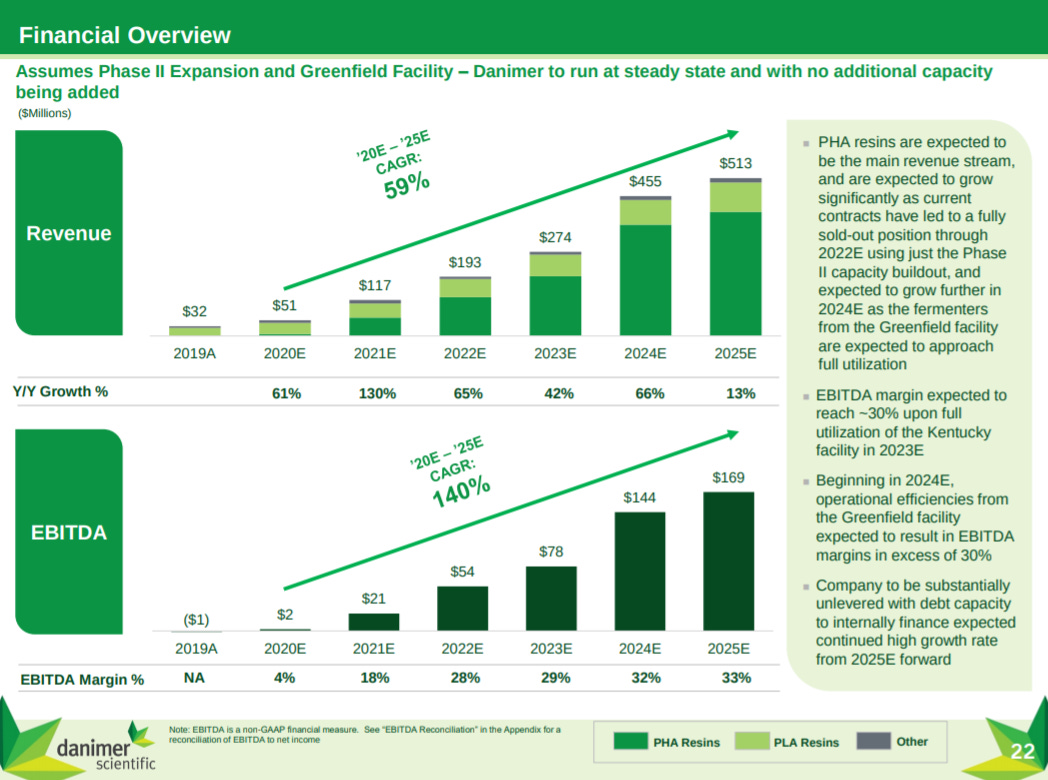

To wrap up the previous two slides, Danimer provides highlights on the deal: raising the capital to get to over $160M in EBITDA in ~5 years.

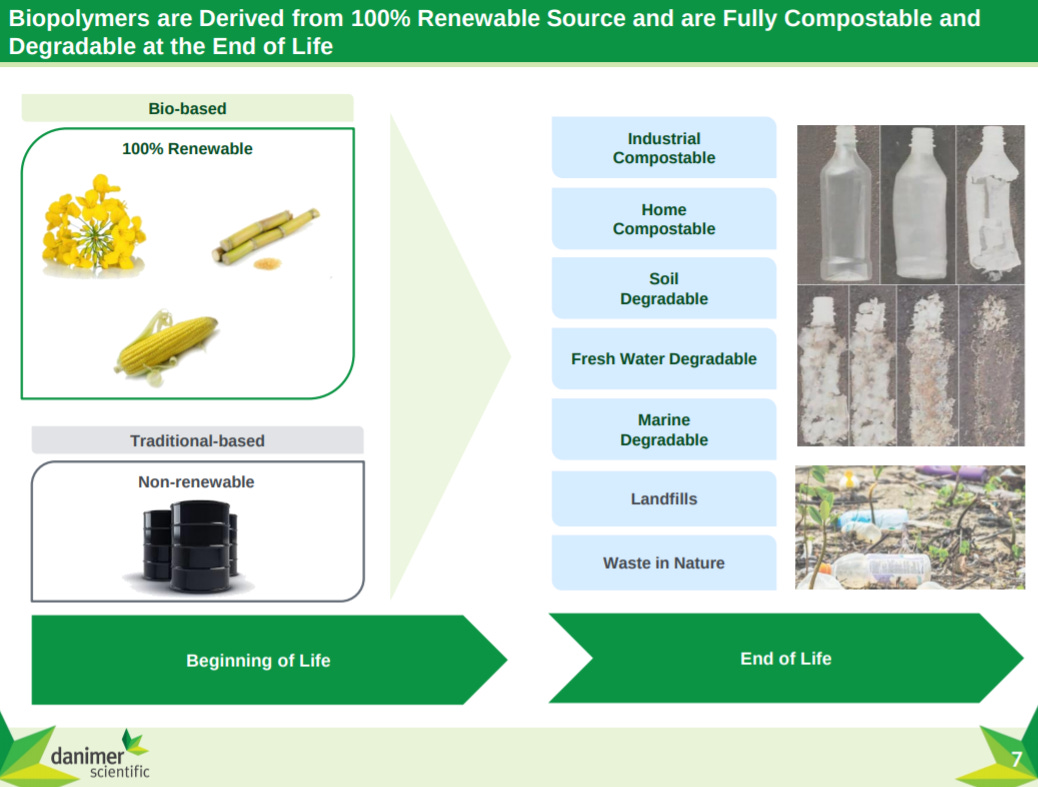

After describing the SPAC transaction, the company describes the advantages of biopolymers versus traditional products - sourced from biosources and are biodegradable.

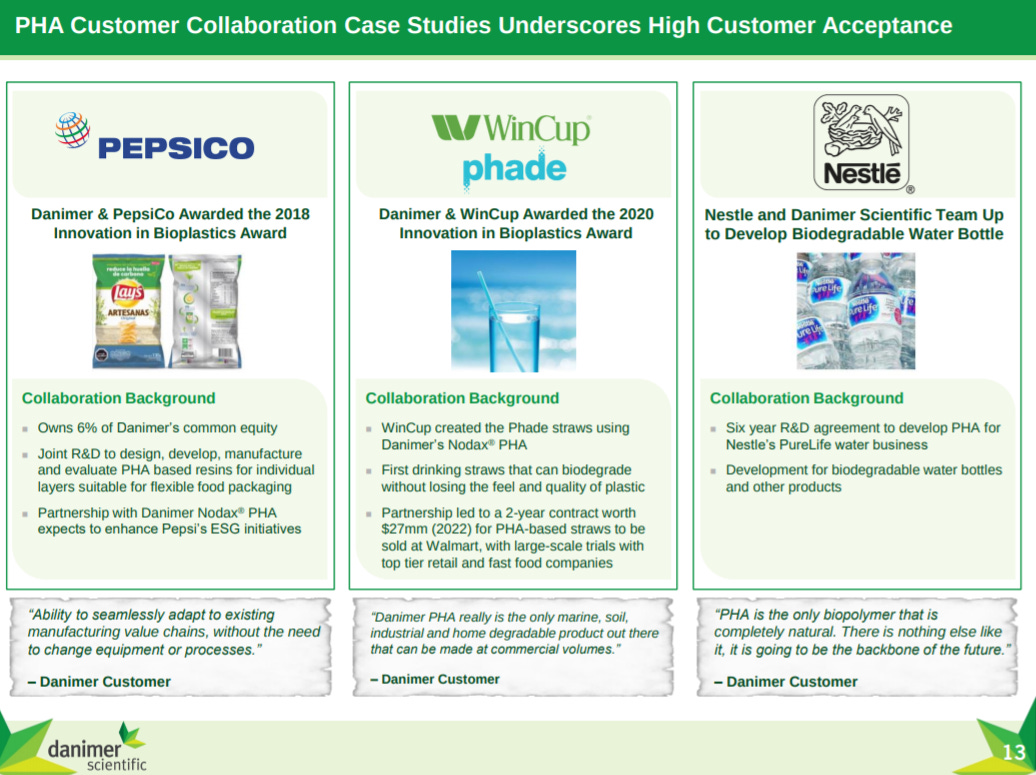

This slide goes into the company’s history. The breakthrough for Danimer was a 2015 designation of Nodax’s marine biodegradability, which set up a deal with PepsiCo a year later with several other commercial deals over the last few years.

The next slide describes Danimer’s market opportunity: over 800B lbs of plastic produced per year with 17B lbs put into the ocean driving the microplastic problem. With under 10% of all plastics recycled in the US, Danimer’s product can be a major driver to reduce the amount of plastic in landfills and the ocean.

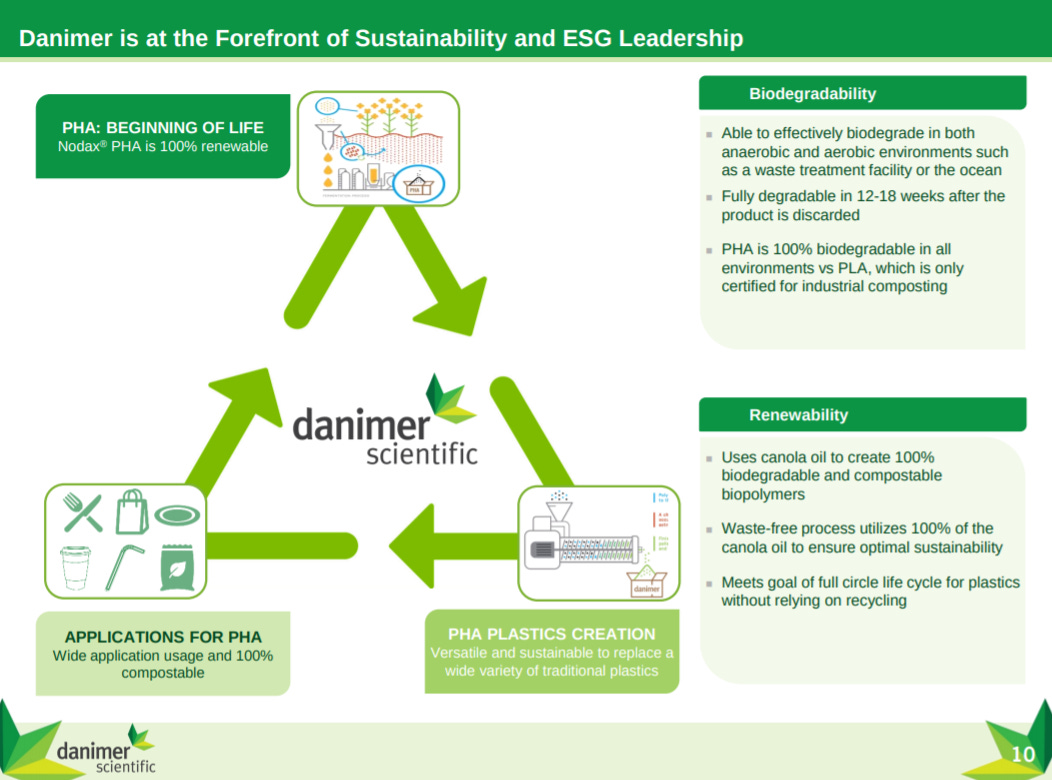

Moreover, supply chain sustainability is important - for Danimer their PHA product can be recycled through the environment while hopefully minimal negative impacts.

The company’s goal is to have around $500M in revenue, about 10x than current levels.

Wit this growth mainly driven by corporate sustainability initiatives.

This slide gives 3 customer case studies starting with the PepsiCo deal in 2017.

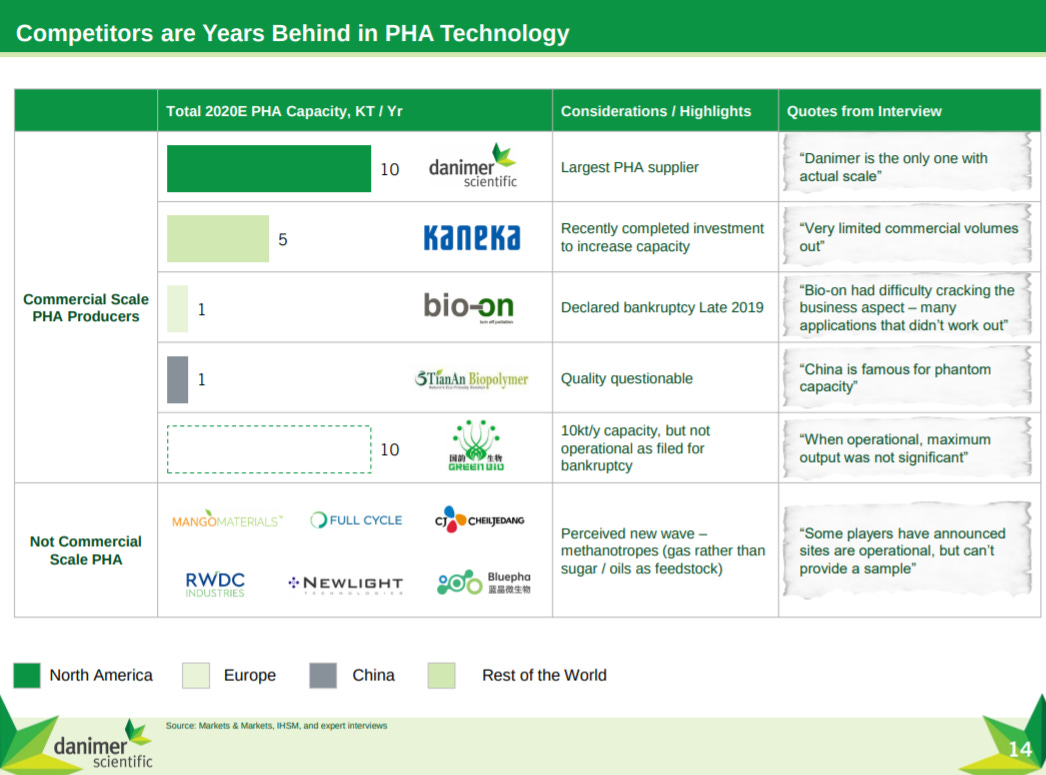

This slide shows Danimer’s leadership position in PHA production. The company has 2 facilities with over 200K total square feet.

With over 40M lbs of PHA lined up for purchase - 760B more lbs to go.

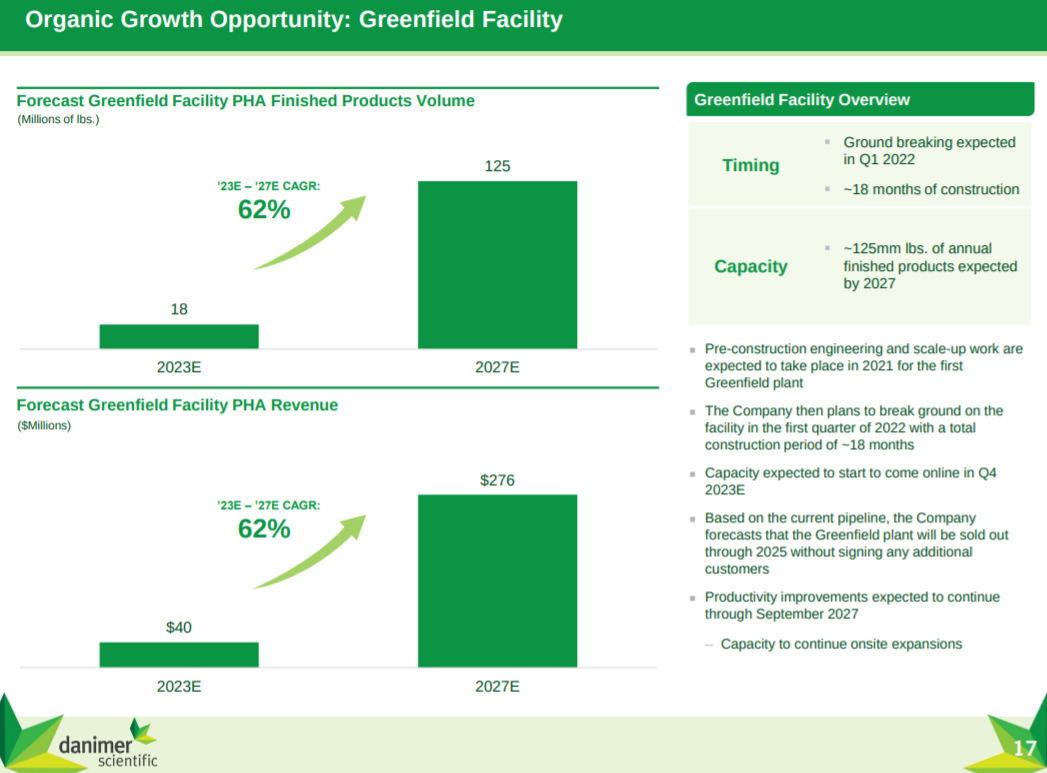

Growth driven by investments into the company’s PHA facility in Kentucky to double Danimer’s manufacturing capacity.

This will drive growth to over 100M lbs of PHA produced per year and $100Ms of annual revenue.

Danimer has fully sold out its PHA capacity until 2022.

The team slide is shown - a lot of people with experience in operations and acquisitions.

This slide again shows the SPAC transaction details valuing Danimer at $890M at the time.

A financial overview to get to $500M in revenue and ~$160M in EBITDA by 2025.

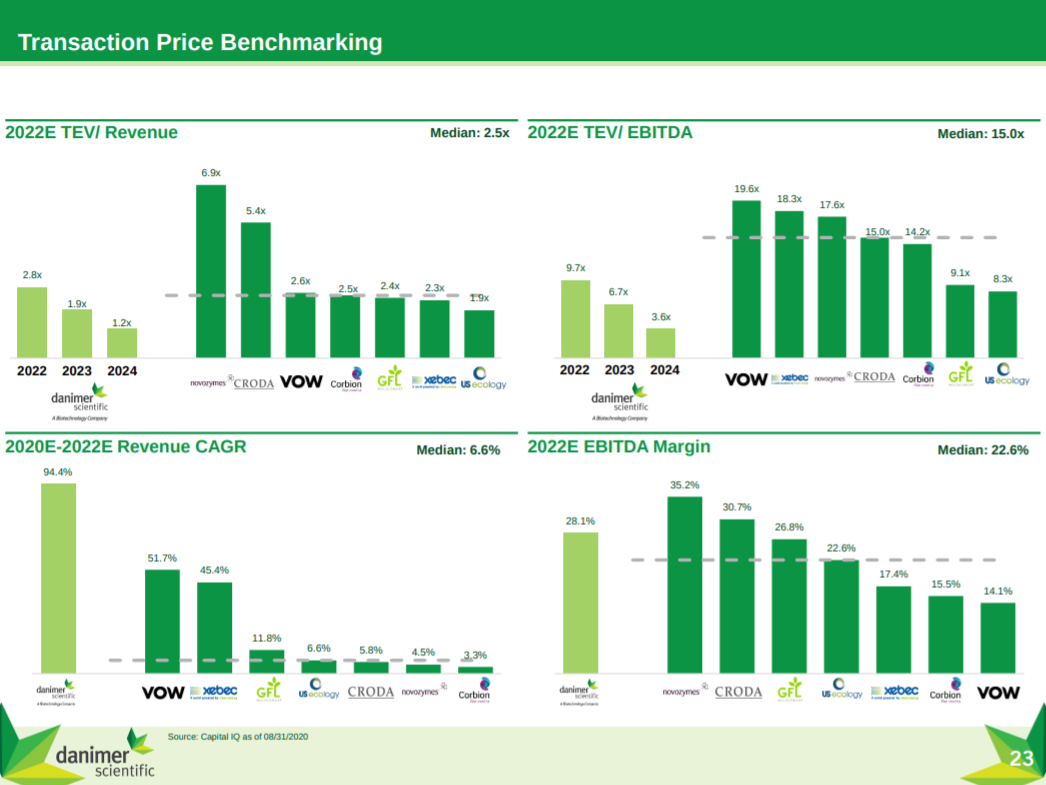

And slide on comparable valuation.

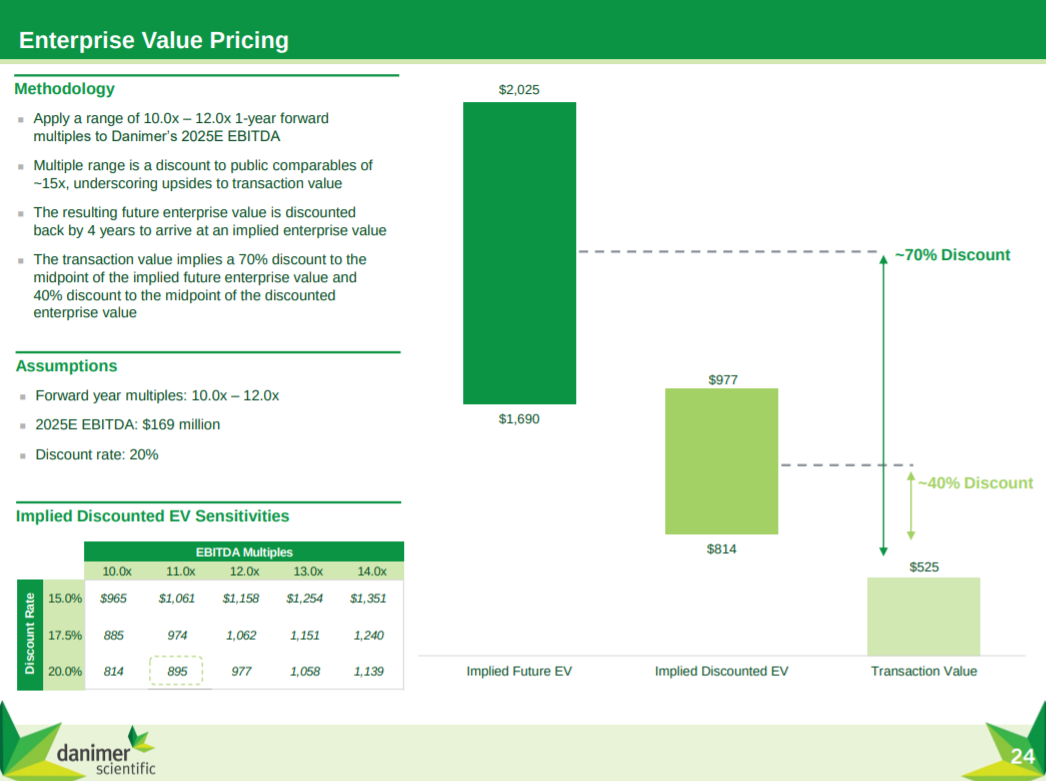

Leading to their valuation on Danimer’s equity.

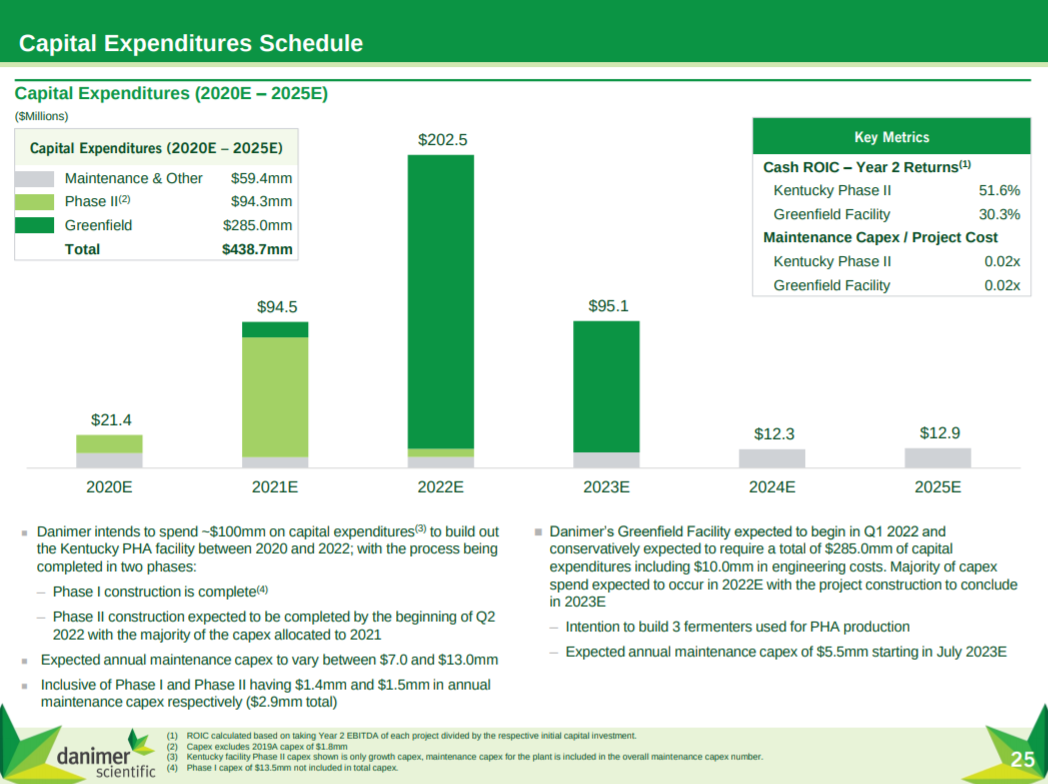

Moreover, Danimer is spend around $300M in cash in efforts to expand capacity and fill corporate demand.

The highlights slide is shown again as a conclusion.

Danimer’s presentation does a good job to show its leadership position in bioplastics and corresponding potential for high sales growth. Deals with corporates like PepsiCo are promising; however, understanding the role of consumer tastes would be useful. The theme of converting agricultural feedstock and waste biomass into bioplastics to reduce carbon dioxide emissions is the key driver for Danimer’s growth. Caveats like landuse and other tradeoffs must be identified and controlled for during this transition, but the opportunity to reinvent supply chains and reduce the amount of plastics in the ocean is so large that Danimer and other companies especially startups have a lot of growth left.

Follow up questions for the team:

What are the regional/country-specific regulations on bioplastics? The US relies on the FDA - others?

What are the key drivers for making PHA/PLA production more energy and resource efficient?

How does Danimer source material? Biomass and/or feedstock?