More well thought out work can be found at — https://axial.substack.com/

Axial partners with great founders and inventors. We invest in early-stage life sciences companies often when they are no more than an idea. We are fanatical about helping the rare inventor who is compelled to build their own enduring business. If you or someone you know has a great idea or company in life sciences, Axial would be excited to get to know you and possibly invest in your vision and company . We are excited to be in business with you — email us at info@axialvc.com

uniQure was founded in 2012 taking over the assets of Amsterdam Molecular Therapeutics (AMT) after the latter failed to get approval for their AAV5 gene therapy, Glybera, for lipoprotein lipase deficiency (LPLD; an ultra-rare disease) in 2011. Forbion Capital Partners led by Sander van Deventer and Philip Astley-Sparke drove the transfer of AMT’s assets into uniQure bringing on board Glybera as well as AMT’s AAV5 license from NIH. uniQure in short is a company built as a recapitalized version of AMT.

Shortly after founding, Glybera was approved by the European Commission in October 2012 under exceptional circumstances. With this early win, the company continued to execute on the strategy AMT laid out focusing on hemophilia B as well as Parkinson’s disease and acute intermittent porphyria.

The first slide of their latest corporate presentation alludes to uniQure’s goal to become a fully-integrated gene therapy company.

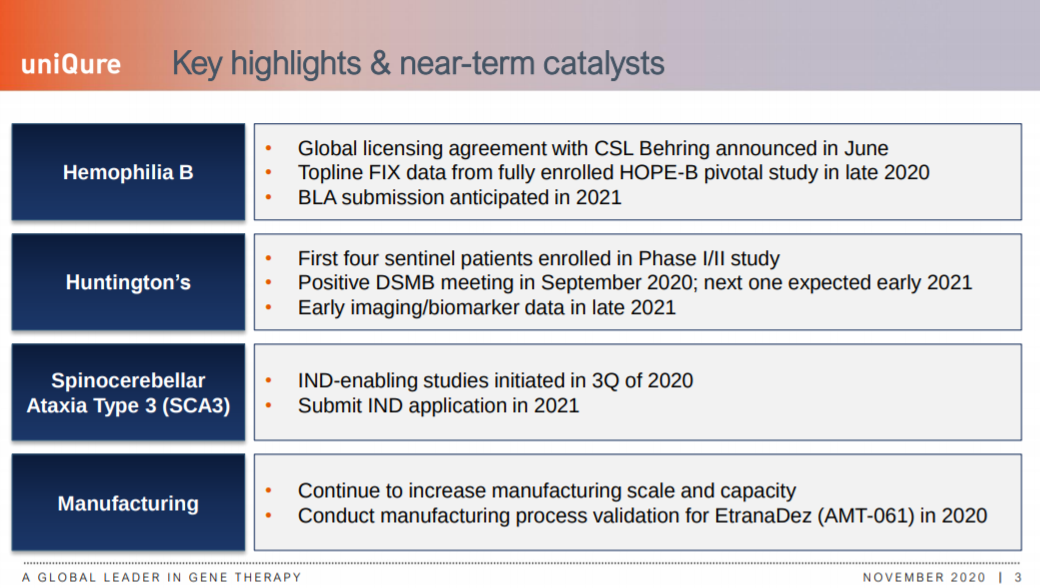

The next slide lays out the key catalysts for the company: (1) licensing out their hemophilia B program to CSL Behring and (2) focusing their attention on developing their own gene therapy for Huntington’s disease.

Along the theme in cell and gene therapy that the process is the product, uniQure explains their core advantage in AAV manufacturing relying on insect cells and one of the largest gene therapy manufacturing facilities in the world. This moat is the result of a major investment on the company’s side over 7 years ago - https://www.biospace.com/article/releases/uniqure-to-build-55-000-square-foot-state-of-the-art-gene-therapy-production-plant-in-u-s-to-leverage-aav-manufacturing-strength-/

uniQure’s pipeline is centered around AAV5, a gene therapy focus with known targeting ability to the brain and the liver. A key part of the company’s founding was acquiring the exclusive AAV5 license from NIH through AMT. Over the last 8 years, uniQure has validated the clinical safety of the vector across 5 studies and even showed the potential for redosing AAV5 gene therapies - https://tools.eurolandir.com/tools/Pressreleases/GetPressRelease/?ID=3335673&lang=en-GB&companycode=nl-qure&v=

Then uniQure goes into their lead asset in hemophilia B.

Controversially, uniQure sold off the majority of their rights to their gene therapy, AMT-061, in hemophilia B to CSL Behring - https://www.cslbehring.com/newsroom/2020/csl-behring-acquires-uniqure-amt-061 uniQure received a $450M upfront payment with $1.6B in milestones ($300M tied to regulatory events and first sales) and tiered royalties up to 20%. This decision will make or break uniQure - it depends on the company’s ability to use the capital to develop new medicines and bring on board new technology. It seems like uniQure wanted to offload the hemophilia asset to focus more on CNS, which probably enables a large biopharma to acquire the company.

uniQure explains the details of the CSL licensing deal.

uniQure explains the logic of the deal: CSL is a leader in hemophilia B and acquiring uniQure for AMT-061 along with the rest of the pipeline didn’t make sense so the second-best option is to license out the asset.

The company explains the market for hemophilia B: the high annual cost of current treatments along with the societal/healthcare burden for each patient make the indiciation a great fit for a potentially curative gene therapy.

AMT-061 is an AAV5 gene therapy focused on increasing levels of Factor IX (FIX) to improve blood clotting in hemophilia B patients. The viral vector delivers the Padua variant of Factor IX (FIX-Padua) a R338L mutation that increases the activity of FIX about eightfold versus wild-type. Using this variant is the key breakthrough for why gene therapies in hemophilia B have seen more clinical success because past gene therapies delivering wild-type FIX could never get beyond 5% normal activity.

Across 10 patients, AMT-061 (seems to be a type on the slide) is increasing FIX expression levels over 5%.

For 3 patients, they have observed significant increases in FIX activity over a year.

uniQure explains their pivotal phase 3 trial for AMT-061.

After explaining their logic to license out AMT-061, uniQure goes into their current lead asset focused on Huntington’s disease.

Huntington’s disease (HD) has only one approved treatment (for symptoms, not the pathology) despite the cause of the disease being known: trinucleotide expansion of an exon in the huntingtin gene.

uniQure describes their gene therapy for HD: delivering microRNAs (miRNA) to inhibit the production of the mutated form of the huntingtin (mHTT) protein.

The company lays out the preclinical progress for AMT-130.

Then uniQure adds a slide on the pathology of Huntington’s disease.

This sets up data in non-human primates where they show the distribution of AMT-130 reaches key sites in the brain driving the pathology of HD.

uniQure shows preclinical data from minipig models for HD where mHTT levels decrease over time within most regions of the brain.

Mice data shows that the AMT-130 restores some neural functions.

In mice, AMT-130 lowered levels of both HTT and exon1 HTT mRNA.

With this preclinical data package, uniQure is planning to initiate a phase 1/2 clinical trial for 26 HD patients.

This slide goes into the phase 1/2 clinical trial design.

Then endpoints for the trial.

uniQure’s penultimate slide is focused on their pipeline. The outcome of the licensing deal as well as the progress for AMT-130 will make or break the company. This is a polarizing decision for the team to make.

The company ends the presentation showing their catalyst slide again.

uniQure’s deck does a great job explaining their advantages in AAV gene therapy manufacturing and does their best to validate their logic of licensing out their hemophilia B asset and focusing on Huntington’s disease. They could use a team slide.

Follow up questions for the team:

Is uniQure focused on rebranding as a CNS gene therapy company?

Given the company’s unique manufacturing capabilities, is CSL Behring paying a services fee for AMT-061 or is this already baked into the licensing agreement?

What type of transactions can uniQure execute given the company’s exclusive license on AAV5?